For some background on this monthly publication, here is my view on dividend growth stocks:

Dividend growth stocks aren’t always the most exciting investments out there. They often aren’t grabbing the headlines, and they aren’t the stocks running up hundreds of percentages in a year. In fact, they are often some of the least exciting stocks. And that is precisely their strongest selling point. With such a vast world of dividend growth stocks available out there, it is important to screen through to see if there are any worthwhile investments to explore.

They are stocks that provide growing wealth over time to income investors. Dividend growers are often larger (not always), more financially stable companies that can pay out reliable cash flows to investors. Some are slower growers than others. Some are going to be cyclical that require a strong economy. Some are going to be secular, which doesn’t generally rely on a more robust economy.

Dividend growth can promote share price appreciation. Of course, that is if these companies are growing their earnings to support such dividend growth in the first place. Trust me. There are yield traps out there – I’ve owned a few that I’m not particularly proud of.

I like to think of investing in dividend stocks as a perpetual loan of sorts. Essentially, every dividend is a repayment of your original capital. Eventually, holding long enough, you have the position “paid off.” It is all returned back into your pocket from that point forward.

All of this being said, it is important to understand my approach to dividend stocks and why screening dividend stocks can be important for income investors. As with any initial screening, this is just an initial dive – more due diligence would be necessary before pulling the trigger.

The Parameters For Screening

I’ll be using some handy features that Seeking Alpha provides right here on their website for this screen. In particular, I will be screening utilizing their quant grades in dividend safety, dividend growth and dividend consistency.

Dividend Safety is relatively self-explanatory. These will be stocks that SA quants show reasonable safety compared to the rest of their various sectors. The grade considers many different factors, but earnings payout ratios, debt and free cash flow are among these. This category will be stocks with A+ to B- ratings.

For the dividend growth category, we have factors such as the CAGR of various periods relative to other stocks in the same sector. Additionally, the quants also look at earnings, revenue and EBITDA growth. As we will see, this doesn’t mean that every stock with a higher grade has the growth we are looking for. This just factors in that the dividend has grown or earnings are growing to support possible dividend growth. For these, the grades will also be A+ through B- ratings.

Finally, for dividend consistency, we want stocks that will be paying reliable dividends for us for a very long time. In particular, hopefully, they are raising yearly, though that isn’t an explicit requirement. We will also include stocks with a general uptrend in dividend payments, which means there could have been periods where they paused increases for a year or two.

After looking at those factors alone, we are left with 440 stocks at this time from the 436 listed last month. I’ll link the screen here, though it is a dynamic list that constantly updates regularly. When viewing this article, there could be more or less when going to the link.

From there, I wanted to narrow down the list a lot more. I then sorted the list by forward dividend yield, from highest to lowest. Since these will be safer dividend stocks in the first place, screening for those among the higher payers shouldn’t hurt.

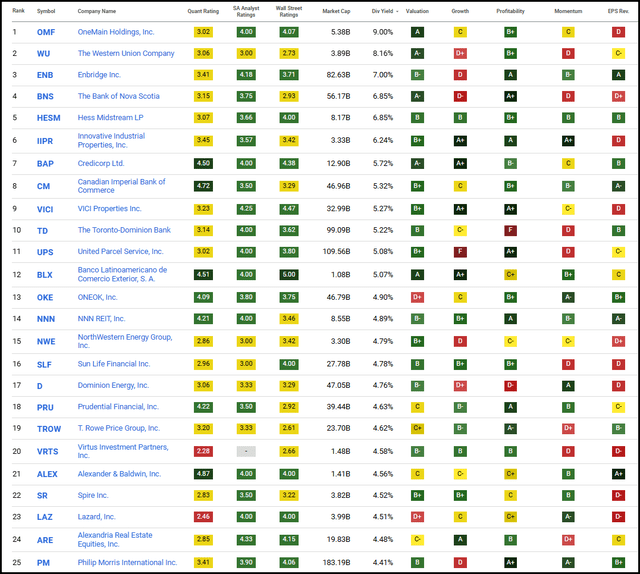

Top 25 Screening (Seeking Alpha)

As usual, we have a few repeats that we have touched on within the last quarter. So, we’ll skip over these names for this month, which include Hess Midstream (HESM), Innovative Industrial Properties (IIPR) and Canadian Imperial Bank of Commerce (CM).

We also have two names that we will skip over, as I don’t believe they are achieving the consistent part in dividend growth. That is The Western Union Company (WU) and Credicorp (BAP).

That leaves us with OneMain Holdings (OMF), Enbridge (ENB), The Bank of Nova Scotia (BNS), VICI Properties (VICI) and The Toronto-Dominion Bank (TD).

OneMain Holdings 9% Yield

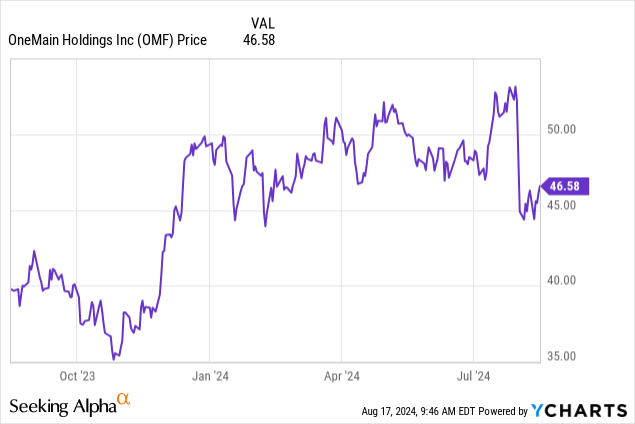

This is a repeated name that comes up quite frequently. This is also one name that I’ve been cautious about due to their reliance on a strong economy and my expectation that the sub-prime borrowers would be pressured sooner than they have been. However, the U.S. economy and the borrowers that OMF lends to with their personal loans have remained incredibly resilient. In fact, we just had OMF’s latest earnings report, and they beat on both the top and bottom line estimates.

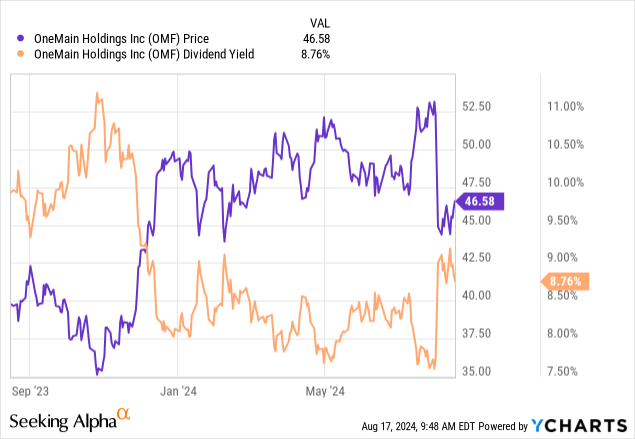

Despite the rather solid results, shares of OMF have been under pressure more recently over the last couple of days. Assuming we aren’t entering into an economic downturn, that simply helps to increase that yield meaningfully.

Data by YCharts

Of course, the risk is always if the company needs to cut its dividend should the economy slow down too much. The company is still really sensitive to the lower-end consumer, given that’s their target market.

With earnings expected to dip lower in the coming year and the share price still rising over the last couple of years—that has pushed the shares to levels that look overvalued currently. At least based on its historical trading range, so while that 8.5x P/E would otherwise look tempting, it suggests it is trading near the higher end based on weaker earnings coming this year.

OMF Fair Value Range (Portfolio Insight)

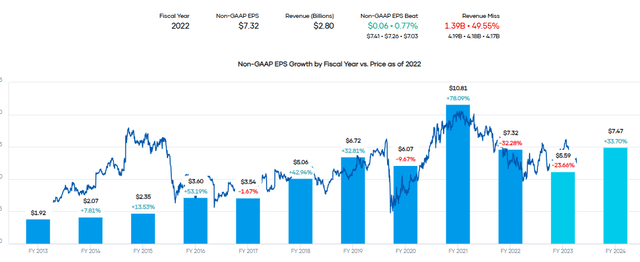

Some may point out that earnings in 2025 are expected to grow significantly, with the analyst consensus reaching $7.48 EPS. However, during our last October publication, I said that the earnings for 2024 looked suspect. At that time, analysts were expecting EPS to reach $7.47.

With earnings expected to drop through this year, some of this is being reflected in the weaker economic outlook expected. Shares are trading at a forward P/E of just 6.7x; it is certainly cheap. However, the expected recovery in earnings into 2024 is suspect, in my opinion. Therefore, I believe it could get cheaper going forward and could be worth picking up when we are in a full recession panic drop when volatility spikes.

OMF Earnings History and Projections (Portfolio Insight (previous article))

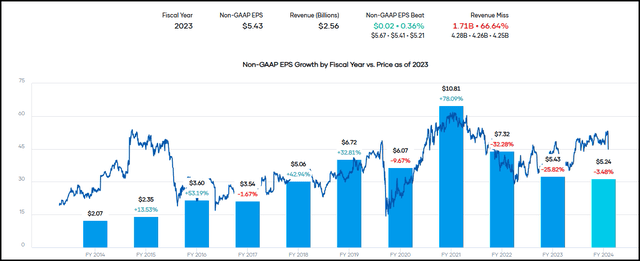

As we are starting to see now that we are into 2024, that assumption that the earnings recovery looked suspect was correct. Analysts are now expecting another slight decline, with EPS for 2024 coming in at $5.24.

OMF Earnings History and Forward Estimates (Portfolio Insight)

They have $2.47 EPS under their belt in the first half, and if they can continue to beat expectations, then the $5.24 looks quite achievable.

On the other hand, I was really wrong when I said that shares could get cheaper—outside of dipping more in the overall October 2023 market sell-off shortly after the original publication—shares were heading higher. Only more recently we’ve seen a pretty harsh sell-off.

Data by YCharts

Overall, in my opinion, this remains a potential speculative position, but it is one I am willing to pass up for now. If I continue to be wrong, and it heads higher, and they keep raising their dividend in the coming years, then I’m okay with that too.

Enbridge 8.16%

ENB, of course, needs little introduction for most energy or income-focused investors. This is a Canadian infrastructure company with a concentration in pipeline operations. Interestingly, we have 3 Canadian companies to discuss today, with BNS and TD also—and we would have touched on CM if we hadn’t done so already in last month’s screening piece.

However, ENB is also more diversified than just pipelines, operating a growing utility business with recent acquisitions and a renewable power generation business. Utilities often can provide more stability in terms of cash flows, and that can result in less risk—which is one of ENB’s selling points for why they are pursuing these utility acquisitions.

The acquisitions that have closed and are expected to close have been helping ENB already. They raised their 2024 EBITDA based on the presumption of closing the PSNC in the third quarter. That said, the liquids pipeline business in Q2 still accounted for almost 57% of the company’s adjusted EBITDA.

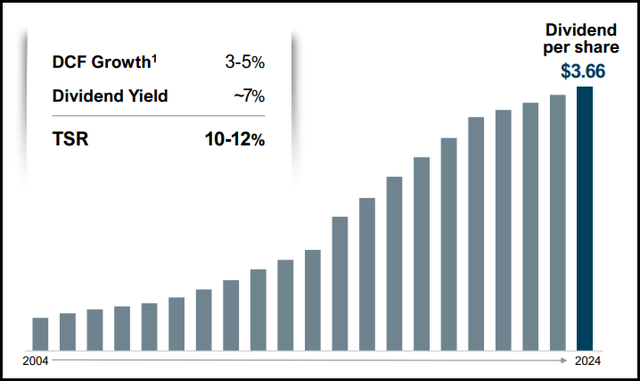

Even without these more stable cash flow cow utility operations, ENB has been able to deliver on the growing dividend front. That isn’t expected to change either going forward, as coverage is strong and distributable cash flows are expected to continue to grow.

ENB Dividend History and Growth (Enbridge Investor Material)

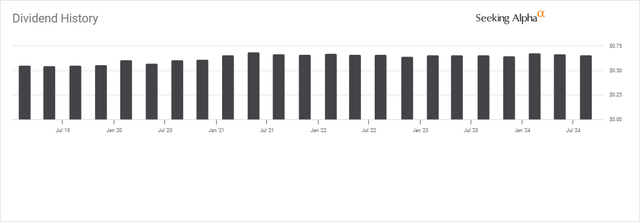

For U.S.-based investors, distributions may look bumpy and like they aren’t growing. However, that has to do with the CAD to USD conversions. That has been a headwind, making the U.S. dividends appear flat for several years now. We’ll see that be the case for the other Canadian companies we touch on today.

ENB Dividend History (Seeking Alpha)

The Bank of Nova Scotia 6.85% Yield

Speaking of other Canadian companies we’ll be touching on today, BNS is the third-largest Canadian bank in terms of total assets. This isn’t a newcomer to our monthly series, but it isn’t one that comes up too often. The last time we touched on this name would be back in July 2023, making it just over one year ago.

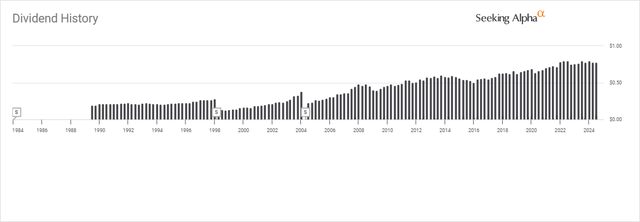

Similar to ENB above, BNS has been increasing their dividend regularly, but for U.S.-based investors, we’ll see something more like this chart below—where the dividend appears to have stalled out over the last several years.

BNS Dividend History (Seeking Alpha)

However, it should be noted that while the dividend has been trending higher, they did choose to pause the increase with the latest announcement. The latest announcement should have been the usual time to announce an increase, which was brought up in the latest earnings call by an analyst:

Mario Mendonca

Okay. And then, again, this is something I may have missed. I thought the cadence for dividend increases was every Q2, but again, I may have missed this. I don’t see a dividend increase this quarter?

Raj Viswanathan

No, you haven’t missed anything, Mario, as always. I think, yes, there is no dividend increase this quarter. It’s part of what we’re thinking is, we do want to grow dividends in line with our earnings growth, which we know is going to happen in 2025, rate situation and other stuff to contribute it. So we decided that it’s better to take a pause at this time and we should start commencing our dividend increases in 2025, in line with what we do every year in the second quarter.

Essentially, they, along with the analyst consensus, don’t expect earnings to grow this year, so they are holding steady with the current payout. That isn’t something that should be seen as too much of a negative—perhaps even more companies should adopt this sort of strategy of freezing dividend hikes when it can help strengthen the balance sheet.

For my dividend growth plays, while I like the consistency of raising every year, but it isn’t really a requirement for me—as I also believe the raises should be warranted. I don’t mind if companies I own take a pause for a year or two or just keep more modest increases. As long as the trend is rising over time, I’m content.

BNS is expected to see earnings growth return in fiscal 2025 and 2026, and as they mentioned above, they can revisit growing the dividend then.

BNS Earnings History and Forward Estimates (Portfolio Insight)

VICI Properties 5.27% Yield

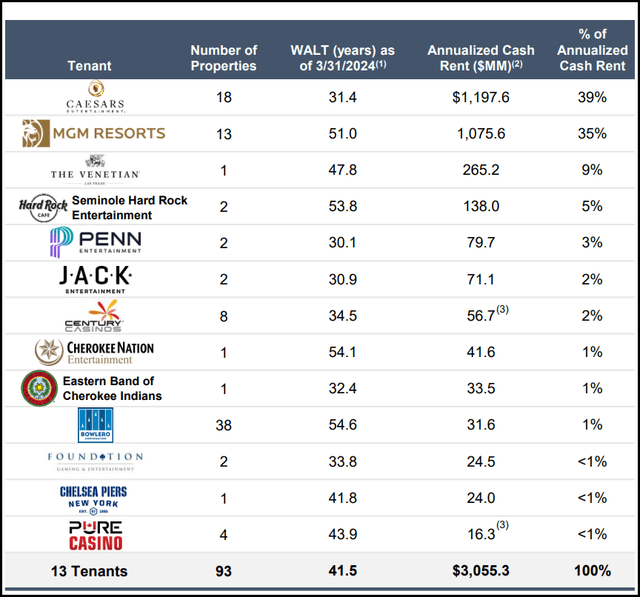

VICI is another popular income investor favorite, though a little less under the radar than ENB, as it doesn’t have quite the history. This is a real estate investment trust (“REIT”) focused on experiential assets, with a particular concentration on casinos that contribute the overwhelming bulk of their annualized cash rent.

VICI Tenant Exposure (VICI Properties Investor Material)

The concentration here is something that, I believe, makes VICI riskier but not necessarily too risky to own, as I do own a position in this name. I’ve utilized the options wheel strategy on VICI several times now; that involves selling put options, taking assignments, and then writing covered calls.

Currently, VICI is in an uptrend, and I wrote some covered calls to collect some added ‘income’ along with the quarterly dividend. The next quarterly dividend is also expected to be when they increase their payout to investors as well; that is, if management sticks with the historical cadence in what is admittedly a fairly limited history.

VICI Dividend History (Seeking Alpha)

With funds from operations (“FFO”) expected to continue to grow in the next couple of years and a modest REIT payout ratio of ~65%, I don’t see lifting the dividend being a problem either.

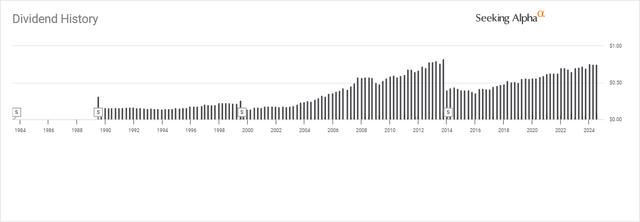

The Toronto-Dominion Bank 5.22% Yield

Finally, we have TD, another Canadian financial institution, to touch on today. This is the first time TD has made the discussion portion of this monthly series. In terms of size, this bank rivals the Royal Bank of Canada (RY) for the top slot for largest Canadian banks in terms of total assets but comes in just shy, taking the second spot.

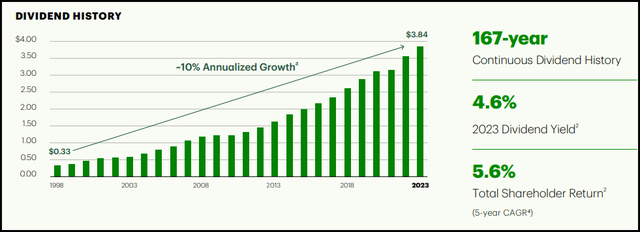

In the company’s 2023 annual report, they boasted about 167 years of continuous dividend history. That includes a rising dividend over the last 25 years—though they did freeze the payouts during the Global Financial Crisis and during the Covid pandemic for understandable reasons. Again, I believe that just goes back to being prudent and protecting the balance sheet in uncertain times trumping getting that raise in every single year.

TD Dividend History (TD Investor Material)

For U.S investors, this has looked more like this being the dividend history:

TD Dividend History (Seeking Alpha)

(The dividend amounts have not been adjusted for the 2-for-1 stock splits in 1999 and 2014.)

Earnings are expected to be softer in 2024, similar to BNS, and that followed a decrease in FY 2023. However, going into 2025 and 2026, we see that earnings are expected to start rising once again.

TD Earnings History and Forward Estimates (Portfolio Insight)

In fact, these analysts’ consensus estimates for percentage growth are almost identical to what we saw for BNS above. With solid dividend coverage based on the ~50% earnings payout ratio, TD’s dividend looks quite secure. For context, BNS’s dividend payout ratio comes closer to ~67% based on forward estimates. Considering that, it could have played a role in why BNS decided to freeze the dividend where it was this year.

This article was written by Follow Value-oriented ideas and special situations, generally mid/small cap. Also, orphaned and unfashionable investment ideas, ideally with a catalyst

This article was written by Follow First Principles Partners is an equity research analyst specializing in technology, innovation, and sustainability investment. My unique approach,