Investment Approach

- Fidelity® Select Industrials Portfolio is a sector-based equity-focused strategy that seeks to outperform its benchmark through active management.

- We believe that uncertainty provides investment opportunity. Stock prices can become disengaged from a company’s intrinsic (fair) value at cyclical extremes because of investor overreaction.

- Cyclical stocks exhibit repeatable patterns. We believe this can present opportunities for a disciplined investor whose time horizon spans the next cycle.

- We strive to capitalize on these opportunities through intensive, academic-style research on cyclical drivers and company-specific fundamentals, along with disciplined portfolio construction. The fund’s success is predicated on finding the right mix of undervalued cyclicals and more consistent earnings growers throughout the cycle.

- Sector strategies could be used by investors as alternatives to individual stocks for either tactical- or strategic-allocation purposes.

|

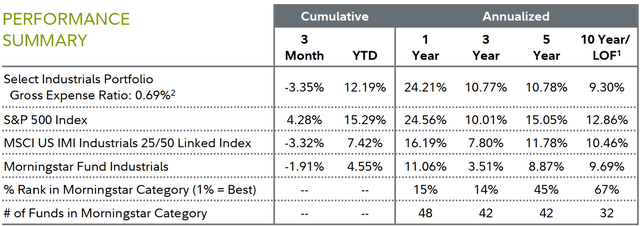

1 Life of Fund (LOF) if performance is less than 10 years. Fund inception date: 03/03/1997. 2 This expense ratio is from the most recent prospectus and generally is based on amounts incurred during the most recent fiscal year, or estimated amounts for the current fiscal year in the case of a newly launched fund. It does not include any fee waivers or reimbursements, which would be reflected in the fund’s net expense ratio. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate; therefore, you may have a gain or loss when you sell your shares. Current performance may be higher or lower than the performance stated. Performance shown is that of the fund’s Retail Class shares (if multiclass). You may own another share class of the fund with a different expense structure and, thus, have different returns. To learn more or to obtain the most recent month-end or other share-class performance, visit Fidelity Funds | Mutual Funds from Fidelity Investments, Financial Professionals | Fidelity Institutional, or Fidelity NetBenefits | Employee Benefits. Total returns are historical and include change in share value and reinvestment of dividends and capital gains, if any. Cumulative total returns are reported as of the period indicated. For definitions and other important information, please see the Definitions and Important Information section of this Fund Review. |

Market Review

For the three months ending June 30, 2024, the industrials sector, as measured by the MSCI U.S. IMI Industrials 25/50 Index, returned -3.32%, while the broad-based S&P 500® index finished with a 4.28% gain. After shaking off a rough April, the broader market rose in May and June, but the rally was mainly confined to certain stocks in the information technology and communication services sectors.

Resilient corporate profits, a frenzy over generative artificial intelligence and the Federal Reserve’s likely pivot to cutting interest rates later this year were factors driving the narrow advance. Only three of 11 sectors topped the broader market in Q2, and industrials was one of six sectors that lost ground while the S&P 500® was hitting a series of new all-time highs.

Investors’ emphasis on a narrow group of growth stocks over cyclical and value shares resulted in most industry groups in the MSCI sector index producing lagging returns for the quarter. For example, aerospace & defense – the segment with the largest weighting in the MSCI index – advanced 3%. Within that group, Boeing (BA) finished with a -6% result, while TransDigm Group (TDG) and Raytheon Technologies (RTX) were each up about 4%. The long-term fundamental outlook for commercial aerospace companies is supported by the expected growth in the global commercial jet fleet from 26,750 aircraft in 2023 to 50,170 in 2043. However, jet manufacturer Boeing has struggled to improve supply chain reliability in the wake of pandemic-related labor turnover. Meanwhile, uncertainty over the likely course of U.S. defense spending in a presidential election year resulted in mixed results for Lockheed Martin (LMT) (+4%), Northrop Grumman (NOC) (-9%) and General Dynamics (GD) (+3%).

Industrial machinery & supplies & components, another sizable segment of the MSCI sector index, returned -8% the past three months. Notable index components in this group included Illinois Tool Works (ITW) (-11%), Parker Hannifin (PH) (-9%) and Fortive (FTV) (-14%). An overall weak U.S. manufacturing segment, as evidenced by consistently soft readings in the ISM Manufacturing PMI, has hampered companies in this group.

Turning to a short-cycle group, cargo ground transportation (formerly trucking), with a return of -14%, was the weakest-performing industry in the MSCI index. The group continued to be challenged by a subpar freight market. Thus, even bellwether Old Dominion Freight Line (ODFL) posted a weak -19% result, and Saia (SAIA) checked in with the same return. XPO (XPO) (-13%) and Knight-Swift Transportation (KNX) (-9%) both did somewhat better.

Performance Review

For the second quarter, the fund returned -3.35%, about in line with the fund’s sector benchmark, the MSCI U.S. IMI Industrials 25/50 Index, but trailing the S&P 500®.

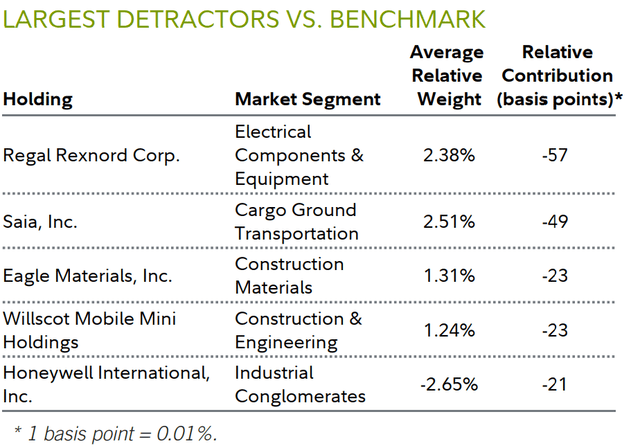

Turning to the fund’s performance, a sizable overweight in cargo ground transportation was one headwind during the quarter, along with stock selection in electrical components & equipment.

Topping the fund’s list of individual relative detractors was Regal Rexnord (RRX), a manufacturer of industrial powertrain solutions, transmissions and electric motors. The stock returned about -25% the past three months. On May 6, the company reported lackluster quarterly revenue and earnings that were largely in line with or below many analysts’ expectations, as demand for the company’s products was disappointing amid a challenging economic backdrop. We slightly trimmed the position, but it remained a core overweight at quarter end.

Also detracting was an out-of-index stake in Eagle Materials (EXP), a manufacturer of construction materials such as cement and wallboard. Our position returned -20% for the three months. In May, the company reported a roughly 17% decline in quarterly earnings, lagging analysts’ expectations, with management citing a lower profit margin in the cement business. We roughly halved the portfolio’s share count here.

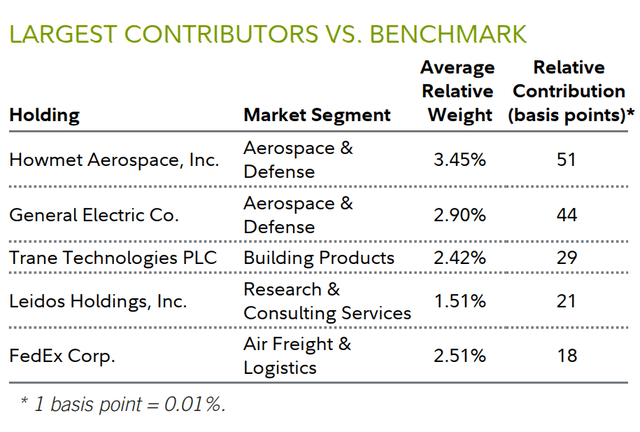

Conversely, stock picking and an overweight exposure to aerospace & defense provided a boost to the fund’s relative result. Picks in trading companies & distributors helped as well.

In stock-specific terms, the fund’s top relative contributor was Howmet Aerospace (HWM). Shares of the jet engine components maker gained about 14% in the second quarter. In May, management reported Q1 financial results that exceeded expectations, including all-time-high revenue driven by a considerable increase in commercial aerospace sales, stemming from record aircraft-manufacturer backlogs. Consequently, management favorably revised its expectations for both earnings and revenue for the full year. Although we trimmed this position, Howmet Aerospace was the fund’s second-largest overweight at quarter end.

Outlook and Positioning

Key indicators reflecting the health of U.S. manufacturers continued to reflect weak demand, with the June reading for the ISM Manufacturing PMI settling at 48.5. Most readings since the third quarter of 2022 have been below 50, traditionally considered the dividing line between expanding and contracting manufacturing activity. After such a protracted period of weak readings, we think it makes sense to look for areas of the industrials sector that could be poised for improvement.

While we remain aware of the macro uncertainty that exists as of mid-2024, we like the fund’s exposure to longer-cycle subsectors and companies tied to themes such as the improving aerospace cycle, as well as reshoring, upgrading the power grid and addressing climate change. The portfolio also holds some short-cycle plays geared to potential improvement in U.S. economic activity.

Industrial machinery & supplies & components was the fund’s largest subindustry overweight as of quarter end, given our expectations for improving demand there in a normalizing economy. Several stocks in this group were among the portfolio’s largest individual overweights as of June 30, including Ingersoll Rand – our top overweight overall – ITT (ITT), Parker Hannifin, Dover (DOV) and Chart Industries.

Cargo ground transportation was another group in which the fund carried a sizable overweight stake at the end of June. Noteworthy holdings here included Saia and Knight-Swift Transportation. These are short-cycle companies that should be early beneficiaries of an improving economy.

Aside from human resource & employment services, which we avoided completely in favor of other groups where we saw stronger growth potential, noteworthy subindustry underweights included construction machinery & heavy transportation equipment. The fund’s only holding in this group was Caterpillar. We are reluctant to invest more heavily here until we see better economic growth in China, where much incremental demand for this segment comes from. The fund was also meaningfully underweight industrial conglomerates at quarter end, although this was partly due to General Electric’s departure from that group as a result of its restructuring moves.

The portfolio’s top-three individual overweights as of June 30 were Ingersoll Rand (IR), Howmet Aerospace and ITT. The three largest underweights at quarter end were Honeywell (HON), Raytheon Technologies and United Parcel Service (UPS).

As always, we thank you for your confidence in Fidelity’s investment-management capabilities.

Read the full article here