Investment Thesis

The Amplify Etho Climate Leadership U.S. ETF (NYSEARCA:ETHO) provides investors with diversified total market exposure to climate-friendly U.S. stocks that pass a rigorous five-level positive and negative screening process. However, I discovered that while ETHO’s selections score well on ESG factors, the fund’s quality features are questionable, given how 15% of the fund’s holdings by weight have negative net income margins. As a result, it’s more speculative than other ETFs like the iShares Climate Conscious & Transition MSCI USA ETF (USCL) and the US Vegan Climate ETF (VEGN), which, I believe, are better long-term buys. Ultimately, ETHO is a “sell”, and I look forward to explaining why in further detail below.

ETHO Overview

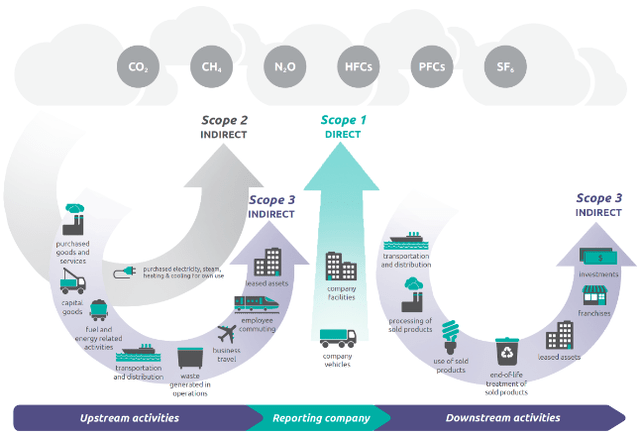

According to Amplify Investments, ETHO “is the first diversified index ETF that avoids fossil fuel companies while selecting equities based primarily on full-Score 1-3 carbon footprint and overall ESG alignment”. The graphic below from the U.S. Environmental Protection Agency describes these three scopes, which fall under the “direct” and “indirect” emissions categories.

U.S. Environmental Protection Agency

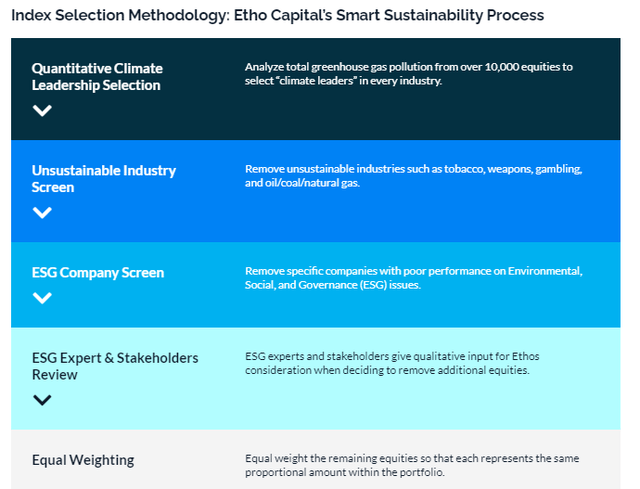

ETHO’s Index ranks companies based on their climate-friendliness across the entire lifespan of their products and services. Selecting these types of companies are the Index’s positive screens, while excluding ones in so-called “unsustainable” industries and those with poor performance on ESG issues are the negative screens. The high-level selection process, described by Amplify Investments, is summarized below.

Amplify Investments

One unique feature is the ability for ESG experts and stakeholders to make subjective decisions to remove additional equities, which is reasonable. Although potentially outdated, a study by Research Affiliates noted only a 0.38-0.72 correlation of Company ESG Ratings as of December 31, 2017. Moreover, the researchers found that many metrics are “qualitative in nature,” and translating them “into a numerical quantity largely depends on the provider’s algorithm.” Therefore, I have no issue with ESG experts taking a second look to confirm the selections make sense.

Research Affiliates

Still, it doesn’t appear that the Index uses any financial screens, which puts investors in the challenging position of choosing between being socially and environmentally friendly and earning an adequate return. Since December 2015, ETHO has trailed the SPDR S&P 500 ETF (SPY) by 2.62% per year, translating to a 54.26% difference in total returns.

Portfolio Visualizer

Meanwhile, the iShares ESG Aware MSCI USA ETF (ESGU) was much more competitive at 13.37%. Ironically, it’s the most popular ESG fund on the market because it doesn’t deviate much from SPY (74% total overlap by weight). This finding suggests investors want to be socially friendly, but only if it won’t impact returns.

I’m not surprised by this. Everyone has financial obligations, and it’s concerning when an Index does not include financial screens and seemingly assumes top-performing companies will also be climate-friendly. The table above also indicates that ETHO’s selections are more volatile than the broader market, so I get the impression it’s a very niche product that’s unlikely to appeal to most investors.

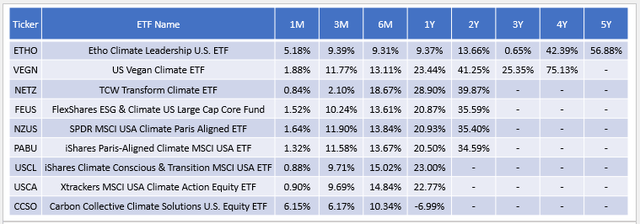

Lastly, consider ETHO’s performance through July 2024 against other climate-focused ETFs over the last five years. ETHO might be the first to market, but these results suggest there are better choices. VEGN has outperformed by 33% over the last four years, while USCL also did well over the last year.

The Sunday Investor

ETF Analysis

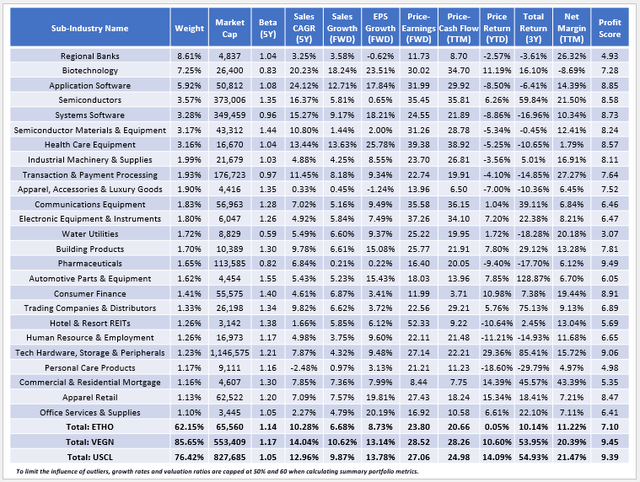

The following table highlights selected fundamental metrics for ETHO’s top 25 sub-industries, comprising 62.15% of the portfolio. I’ve also included summary metrics for VEGN and USCL at the bottom.

The Sunday Investor

ETHO’s 7.10/10 sector-adjusted profit score, supported by weak 11.22% weighted average net margins, is a major red flag. As I mentioned in my investment thesis, 15% of ETHO’s holdings are non-profitable over the last year, and if I had to pick one reason it’s lagged behind its peers in recent years, it’s poor quality. The table shows a weak 4.93/10 profit score for Regional Banks, ETHO’s most prominent sub-industry, and a favoritism for many small- and mid-cap stocks. The implication is that the most climate-friendly stocks are up-and-comers, which, unfortunately, have not yet proven themselves. In contrast, VEGN and USCL have much larger weighted average market caps and, by extension, better profitability metrics. They also have more significant growth potential, evidenced by 3-5% higher estimated sales and earnings per share growth rates.

Readers must weigh ETHO’s poor quality and growth metrics against its relatively strong value features. The ETF trades at 23.80x forward earnings (17.02x harmonic average) and 20.66x trailing cash flow (12.18x harmonic average), several points cheaper than VEGN and USCL. Overweighting Regional Banks helps, but avoiding many high-priced Technology stocks is the primary driver of ETHO’s favorable valuations.

From a technical perspective, ETHO’s holdings have gained a weighted average of 10.14% over the last three years compared to 53.95% and 54.93% for VEGN and USCL, respectively. These figures support the value argument for ETHO, and its equal-weight approach could provide protection in an intense sell-off of the market’s most liquid stocks. Still, it’s a balancing act. In a “flight to safety,” investors won’t turn to ETHO’s poor-quality holdings, and my investing approach is merely to maximize the odds of succeeding in multiple market environments. As it stands today, ETHO does well on diversification and value but lacks sufficient growth and quality, so it doesn’t interest me.

Investment Recommendation

ETHO offers climate-focused investors a well-diversified portfolio of U.S. stocks that have passed a rigorous ESG screening process. Its 0.45% expense ratio is elevated, but I’m mostly concerned with the apparent lack of financial screens, which create a myriad of quality issues that commonly lead to long-term underperformance. To the Index Provider, I suggest reducing the number of holdings or switching to a modified market-cap-weighting scheme to boost quality, neither of which would compromise the strategy’s ESG objectives.

Unfortunately, the likelihood of these changes happening are slight, leaving investors speculating that many unproven small- and mid-cap stocks with cheap valuations will suddenly outperform the high-quality large-cap growth stocks that undoubtedly are here to stay. That’s not a bet I’m willing to take, so I have assigned a “sell” rating to ETHO and recommend climate investors look closer at the higher-quality VEGN and USCL instead. Thank you for reading, and I look forward to your comments below.

Read the full article here